MEIEA Journal Vol 5 No 1 © 2005 Music & Entertainment Industry Educators Association All rights reserved.

Terrell,

Phillip A. (2005). Decentralization and Growth in the U.S. Music

Industry, An Emerging Paradigm: A Longitudinal Comparative

Analysis. MEIEA

Journal Vol 5 No 1, 33-57.

Decentralization and Growth in the U.S. Music Industry, An Emerging Paradigm: A Longitudinal Comparative Analysis

Phillip A. Terrell, Alabama State University

Introduction

Recently, Taylor and Terrell (2004) published research on economic trends in U.S. music industry capitals. Their findings showed that:

1) despite a slowdown in the rate of growth, U.S. music industry capitals had experienced positive growth rates; 2) despite declining record sales, other sectors of the music industry were growing; and 3) patterns of decentralization were occurring among the cities they studied.

However, the researchers were unable to determine whether or not their data would extrapolate to a nationwide model. The purpose of this study is to determine the amount of decentralization, if any, that has occurred within the U.S. music industry. To this end, this researcher has adopted Taylor and Terrell’s (2004) instrument—with adaptations—for comparison of the entire U.S. music industry to the nation’s music industry capitals.

What is the significance of decentralization within the music industry? Put simply, decentralization is becoming a worldwide business trend; it is also reported to be occurring within the music industry. If decentralization is occurring, there are salient implications for both the music industry and its customer base.

Much has been written about the changing face of the music industry and what the future holds for it. There is no shortage of commentary concerning the issue of how the internet is changing the so called arcane business model that has defined the music industry. Perhaps the most succinct observation relevant to this study comes from André Gray, CEO and founder of the Digital and Electronic Music Organization.

When musicians discovered the Web in the early 1990s, it was apparent to them that they had finally found a medium that could quite possibly liberate them from the shackles of the music industry parasites. It did! For the last seventy years, the music industry has basically the same business model that allowed them to control the manufacturing and distribution of music. And the old adage in Hollywood concerning distribution is true: whoever gets their hands on the money first keeps most of it. For the very first time in music business history, the recording artists could have total control over their creative works and, at the same time, have a direct and interactive connection with music fans from around the world. This is by far, the single biggest change the music industry has ever seen since the creation of rock ’n roll […] Because of the advent of legal and illegal digital music, the music industry will no longer be centralized. The decentralization of the music industry is the greatest thing that can ever happen to musicians (Gray 2004).

This study is intended to determine, through a quantitative comparative analysis of current economic trends, whether or not decentralization is occurring within the music industry. To this end, the following definitions provide a contextual frame for the data contained in the methodology section of this work:

Decentralization: the planned, or spontaneous, redistribution of an industry, or industry sector’s, resources (e.g., businesses, employees, and sales) from a state of relative spatial concentration to a more disbursed condition (Terrell 2005). Growth rate: The rate of increase in size per unit (Webster 1996). Market share: The percentage of the market for a product or a service that a company provides (Webster 1996). Music industry (MI): The nine business sectors contained in this study. Music industry (MI) capitals: New York, Los Angeles, Chicago, Nashville, and Atlanta (Taylor and Terrell 2004).

Per capita share: The percentage of businesses, employees, or sales that a company, or industry sector, possesses based upon population (Terrell 2005).

Is the music industry decentralizing? A proper examination of this question should begin with a consideration as to what industrial decentralization is, what factors precipitate this phenomenon, and whether the music industry has experienced decentralization in its past. A brief review of scholarly analysis and trade commentary provides context for this discussion.

Review of the Literature

The phenomenon of industrial decentralization has been an object of study by a significant number of scholars in the fields of business and economics. Additionally, industry insiders and observers have published numerous non-scholarly articles and reports on this subject often touted to be the business paradigm of the twenty-first century. Finally, a modest amount of music industry scholarship has been devoted to decentralization within the discipline.

Industrial decentralization is a concept with origins found in Marxist economic theory. The first generation of Marxist scholars was ardent apologists for industrial decentralization as an alternative to the negatives they observed in the centralized business structures of the industrial revolution. This is exemplified by Kropotkin (1906) who argued that “The tendency of trade, as for all else, is toward decentralization […] diversity is the surest pledge of the complete development of production by mutual cooperation, and the moving cause of progress, while specialization is a hindrance to progress” (p. 251).

In the ensuing years, Marxian decentralization theory developed additional nuances. For example, Krumme (1972), a geographical economist, examined the impact of what he referred to as “spatial decentralization” in industry. His research showed how the Triumph Motorcycle Corporation was able to increase its market share and productivity by moving from a one-plant production facility to a multi-plant inter-regional corporation during the late 1960s. Krumme’s analysis also indicated that regional diversity in a company facilitated extended customer service hours and lowered payroll costs through the attraction of skilled personnel not having to relocate to a centralized facility.

Patrick McGovern, Professor of Information Systems at MIT’s Sloan School of Management, represents the current school of scholarly thought on decentralization in business and technology. In a 2003 interview with Thomas Malone he stated:

The old mode of centralized authority has been severely undermined […] Decentralization is being facilitated by advances in information technology and is enabling decision-making to be far more widely dispersed in both large and small firms. With cheaper communication costs, many more people can make decisions for themselves, because they have the information they need. And when more people make more of their own decisions, they are often more creative, more motivated, more dedicated. That means we’ll be able to have many of the economic benefits of large organizations without having to give up human benefits of smaller ones—things like motivation, creativity and freedom (Malone 2003).

McGovern also sees industry decentralization transforming businesses in diverse sectors. “There is a huge amount of freedom for people at very low levels in the organization. Junior people can make multi-million dollar decisions about technology and even business acquisitions, in part because they have the information in their hands and can easily ask advice from people throughout the company […] companies today are moving away from the rigid, hierarchical ethos that was pervasive in business twenty years ago” (Malone 2003). In Malone’s interview McGovern predicted that “many [of the] things that are done today by large corporations could be done by temporary combinations of very small companies, in many cases even individual freelance contractors. Most people don’t begin to understand yet how important and far-reaching this and other decentralization changes will be” (Malone 2003).

McGovern’s somewhat sanguine analysis that “industrial decentralization will shape the world for the rest of the century” is apparently shared by a significant number of industry insiders and observers (Malone 2003). For example, Kevin Werbach has postulated that “in the coming decade, decentralization will be a critical challenge for the technology, media and telecommunications industries […] Centralized systems are failing for two simple reasons: they can’t scale, and they don’t reflect the real world of people” (Werbach 2002). In the article “Tech’s Newest Trend—Decentrali-zation” Werbach observed that individuals instinctively seek to communicate and collaborate across artificial boundaries of organizations and geography. And, because decentralization inherently breaks down boundaries, it will inevitably cut across multiple industry categories. However, Werbach contends that decentralization is neither automatic nor absolute and that the most decentralized system does not always prevail. He believes that industry’s challenge in the twenty-first century is to find appropriate equilibrium points containing optimum group sizes and viable models with the appropriate social compromises. In his summary, Werbach (2002) states, “Although decentralization is a long-term challenge, the good news is that it’s also an opportunity. Businesses that can capitalize on decentralization— as both creators and users of technology—will be best positioned for the future” (Werbach 2002).

Other industry insiders, such as Balovich (2003), have observed that industrial decentralization is no longer restricted within our continental boundaries (e.g., offshore decentralization). In support of his claim he provided a partial listing of major U.S. companies, including IBM, Procter and Gamble, Dell, Microsoft, and Oracle, who have decentralized their operations to other countries. Balovich observed that the benefits of offshore decentralization for these companies included lower wages and the ability to work around the clock due to their presence in other countries.

The first scholarly analysis of industrial decentralization and the music industry was performed by Shore (1983). The researcher’s historical rendering of the music industry showed that technological advancements had precipitated periods of decentralization followed by record label consolidation. Though the primary focus of his research was the impact of the

U.S. major record labels on the international music market, Shore’s discussion of the benefits of a decentralized domestic music industry provide important insight as to how both music and the commerce of music could benefit from a less centralized industry paradigm. Unfortunately, his recommendations for record industry decentralization were somewhat untimely, for his work was published during what Garofalo (1999) identified as a period of consolidation within the music industry.

The next music industry scholar to discuss industry decentralization in the context of his discipline was Garofalo (1999). He provided historical analysis of how forces external to the music industry precipitated tempo-rary periods of decentralization within the industry. Garofalo explained how a policy decision by the U.S. government created unanticipated consequences for the music industry—specifically, the shellac shortage during World War II. This caused a cutback on the number of records that could be produced and led the major U.S. labels to make a strategic decision to abandon production of African-American music. “This decision, coupled with technological advances favoring decentralization, created the conditions in the 1940s under which literally hundreds of small independent labels— among them Atlantic, Chess, Sun, King, Modern, Specialty, and Imperial— came into existence in the United States” (Garofalo 1999, 3). Among the technological advances to which Garofalo referred is the development of low cost analog tape recorders, which were quickly adopted by the aforementioned indie labels (Terrell 2001).

Another technological advancement discussed by Garofalo was the invention of the transistor in the early 1960s. Because the transistor was capable of performing all the functions of the vacuum tube, “this advance encouraged decentralization in broadcasting and recording, which aided in independent production” (Garofalo 1999, 3). The work of this scholar is important to this study for his identification of periods of decentralization within the music industry, specifically the 1940s and 1960s, and the consolidation period that occurred in the 1980s.

The research of Taylor and Terrell (2002) represents the first attempt to identify and quantify decentralization within the music industry. In their concluding remarks, the researchers encapsulate the views of the literature.

The salient findings of this study are [that] decentralization of the music industry, combined with local niche specialization, are replacing the monopolistic model of the previous century. These changes are precipitated by a combination of forces that include technological advances, population shifts, global economy and evolving musical preferences. Implicit in the findings of this study is that the decentralization patterns of the music industry present opportunities for a larger number of cities to develop significant music industry related businesses within their environment (Taylor and Terrell 2002, 257).

Taylor and Terrell’s (2004) subsequent research has led them to more precisely identify the external factors of the current music industry decentralization cycle:

1) Federal Communication Commission (FCC) deregulation policies in radio broadcasting; 2) Internet file sharing; 3) varying business climates among the music industry capitals; and 4) technological advancement in audio recording.

Nevertheless, the researchers’ findings failed to quantify music industry decentralization at the national level.

The body of literature indicates that industrial decentralization is a developing trend in both the world of business and the music industry. The forces that are perceived to precipitate industrial decentralization include:

1) technological advancements; 2) governmental policy decisions; 3) company profitability and productivity; and 4) a need for increased motivation, creativity, and freedom for a company’s employees.

A comparative analysis was performed to determine if the currently perceived decentralization of the U.S. music industry is real, and if it is real, to what extent has decentralization occurred. A description of the data collection procedures and methodology are contained in the following section.

Methodology

Since the purpose of this study is to determine what quantitative evidence, if any, exists in regards to Taylor and Terrell’s (2004), as well as other, claims of possible decentralization patterns within the U.S. music industry, a replication of the aforementioned researchers’ instrument was adopted with the following modifications. A quantitative-comparative analysis was performed on the entire U.S.—all fifty states—and Taylor and Terrell’s five Music Industry (MI) Capitals of New York, Los Angeles, Chicago, Nashville, and Atlanta for the years 2000 and 2003. The nine music industry sectors of this, and the 2004 Taylor and Terrell foundational study were:

1) Recording Studios

2) Artists’ and Entertainment Managers or Agents

3) Entertainers and Entertainment Groups

4) Record and Pre-Recorded Product Outlets

5) Musical Instrument Stores

6) Musical Instrument Manufacturers

7) Licensing, Royalties, and Publishing Services

8) Creative Services

9) Broadcasting Services

As in the previous research, the databases included the 1997 North American Industry Classification System (NAICS) CD-Rom, the 2000 U.S. Census Report, and a research engine and databases from Dun & Bradstreet (DB) for 2000 and 2003. The NAICS database was used to identify and group music industry sectors by statistical index codes (SIC) into the nine industry sectors of the study. The 2000 U.S. Census Report was used to determine total U.S. and individual MI capital populations. The U.S. population figures and the stated populations for each MI capital (which was combined to produce a music industry capital group total) were used for the calculation of per capita share.

2000 U.S. Census Figures

U.S. Population: 281,421,906MI Capitals: 27,868,622 (9.9% of the U.S. population)

The DB engine was loaded with the selected SIC numbers—sepa-rated by year and business sector—for analysis of the U.S. data. The data for the MI capitals for years 2000 and 2003 was taken directly from the Taylor and Terrell (2004) tables.

Limitations of this Study

For the sake of clarity, the scope of this study was limited to nine predetermined music industry categories. Among the music industry categories not included were business entities whose products or services are experiencing significant decline in market share, for example, hi-fi and other acoustic equipment manufacturer/wholesale and services. Support services such as audio cassette duplication services, musical instrument rental services, music education and instruction, and sound and lighting equipment rental were likewise not included due to lack of a significant market share. Finally, two of the most significant growth sectors for the music industry—entertainment legal services and web-based music delivery entities—were not included due to current limitations in the NAICS eight-digit protocols because they tend to overstate activity within these sectors. Therefore, while the results of this study encompass most of the music industry activity within the United States, they cannot be generalized to encompass all music industry activity within the country.

Results

The results of this study indicate that despite having a greater per capita market share than the U.S., MI capitals have lost market share over time. Additionally, the MI capitals show declining growth in four, and no growth in two, of the nine industry sectors of this study. In contrast, the

U.S. experienced positive growth in number of businesses, total employ-ees, and revenues in eight of the nine MI sectors. This quantitative evidence might indicate a decentralization cycle within the U.S. Music Industry.

Table 1 shows that the commercial recording studio sector in the U.S. is up in all three industry sector categories (number of businesses, number of employees, and total sales). The MI capitals likewise grew, but at a comparatively lower rate, in number of number of businesses and number of employees, but declined in total sales (-16.52%). Additionally, the MI capital’s three growth rates (as shown in the columns entitled “Growth in %”) are slower than the U.S. growth rate. As the row entitled “MI Capitals %” shows, the MI capitals have a greater per capita share than the U.S. as a whole (i.e., more than 9.9% of the national total) in all three categories. However, as the same row shows, the MI capitals have lost market share in the three categories since 2000.

The figures for Artists’ Managers and Agents, as found in Table 2, show the U.S. experiencing healthy growth in all three categories. The MI capitals’ growth rates are slower than the U.S. in number of businesses and number of employees, but greater in total sales. As in the recording studio sector, the MI capitals have greater per capita share in all three categories than the U.S. as a whole. Nevertheless, the MI capitals lost market share in number of businesses and number of employees and experienced only modest gains in total sales.

Table 3 contains the data for the live music sector. The figures show that the U.S. experienced significant growth in all three categories. The MI capitals experienced an equivalent growth rate to the U.S. in number of businesses, but they trailed significantly in the growth of employees and revenues. Again, the MI capitals show a greater per capita share in all three categories when compared to the U.S. as a whole. Nevertheless, the capitals show essentially no, or negative, growth in market share for all three categories.

The Record Retail sector, found in Table 4, shows growth in number of businesses nationally, but shrinkage (-4%) in employees, and is essentially flat in sales. In contrast, the MI capitals experienced modest growth in all three categories. Additionally, the MI capitals experienced a modest increase in market share and had greater per capita shares in all three categories. The comparative success of the MI capitals in this sector may be attributable to sales of recorded product via the internet, whose websites are generally maintained at the corporate headquarters of various national record retail store chains.

In contrast to the record retail sector, music retail trends in the opposite direction. Table 5 shows that the U.S. experienced healthy growth in all three categories. The MI capitals also grew in businesses and employees but lost significantly in sales (-53%); consequently, the MI capitals maintained market share in businesses and employees but lost ground in sales. Nevertheless, the MI capitals have a greater per capita share in businesses and employees but drop below the 9.9% floor in sales for 2003. Finally, the MI capitals show a depressed growth rate compared with the U.S. in employees and sales. These figures tend to support perceptions that the urban music store sector is overbuilt and is having difficulty competing with online music retailers in the Midwestern United States (Franklin 2003).

Although music instrument retail was found to be weak among the MI capitals, music wholesale and manufacturing was found to be a healthy sector for all stakeholders. Table 6 shows that the U.S. and the MI capitals experienced significant growth in all three categories. The U.S. had a slightly faster growth rate in number of businesses but the MI capitals’ growth rate exceeds the U.S. in employees and sales. Additionally, the MI capitals saw a 5% increase in market share for employees and sales during this period.

As in the previous sectors, the MI capitals have greater per capita shares in all three categories.

Table 7 contains the data for licensing, royalties, and publishing services. The figures show healthy growth nationally in number of businesses and sales, but a loss (-20.4%) in employees. The MI capitals experienced modest growth in number of businesses and employees, but demonstrated larger growth in sales. Additionally, the MI capitals had substantially greater per capita shares in all three categories. This data lends support to Taylor and Terrell’s analysis that industry consolidation may be occurring within this sector due to the dramatic increases in employees and sales (market share) for Nashville (Taylor and Terrell 2004).

The fields of songwriting, music arranging and composing, music video production, and disk reproduction were, as per Taylor and Terrell’s instrument, included in the sector entitled creative services (Table 8). The results indicate that the U.S. is experiencing healthy growth in all three categories. The MI capitals show faster growth rates in number of businesses and employees, but are lagging in sales. Additionally, the MI capitals made modest gains in market share for the business and employee categories, but they lost ground in sales. However, the MI capitals do maintain a greater per capita share in all three categories.

The sector of broadcasting services (Table 9) includes SIC categories such as specific format radio station time sales, radio consultants, radio transcription services, and music distribution services. Broadcasting services was found to be the most prolific of the industry sectors in this study generating almost half of the nine sectors’ total dollar output. The U.S. exhibited significant growth rates in number of businesses and employees, but registered negative growth (-22.5%) in sales. In contrast, the MI capitals showed more growth in businesses and employees and were less depressed (-7%) in sales. Also, the MI capitals registered modest increases (about 2%) in market share for all three categories. They had greater per capita shares in employees and sales, but failed to reach the statistical average of 9.9% in their number of businesses. These data, which show MI capital broadcasting to be more resilient than the nationwide industry sector downturn, tend to support reports of broadcast industry consolidation as a result of the deregulation of the telecommunication industry by the FCC (Clark 2003). Finally, this is the only industry sector to show negative growth in revenues in this study.

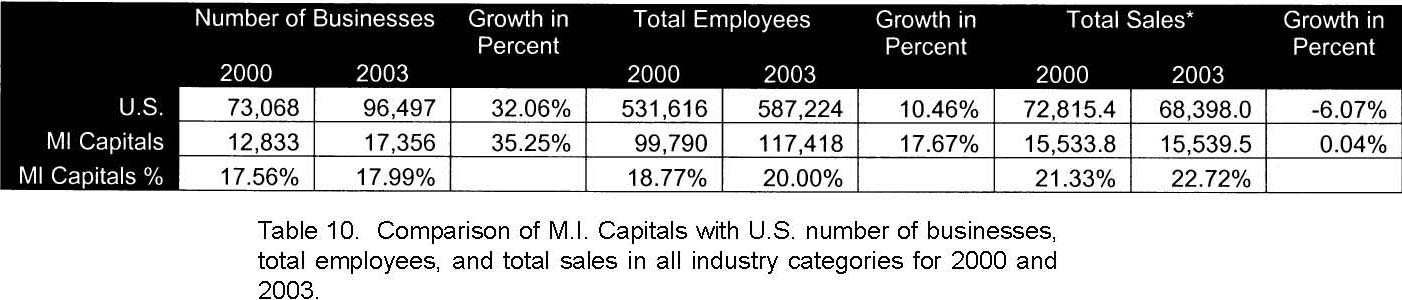

Table 10 contains the totals of the nine sectors of this study. U.S. trends show growth in the number of businesses and total employees but are down (-6%) in sales. It is a testament to the strength of the remaining industry sectors in that they were nearly able to absorb the dramatic loss of revenue experienced by broadcast services, the largest sector. The MI capitals experienced slightly larger growth rates than the U.S. in number of businesses and employees but were flat in sales. However, these combined figures mask the MI capitals’ inability to maintain market share in industry sectors one through eight. This is examined in the next section.

Finally, the figures showing the MI capitals possessing greater per capita shares (i.e., more than 9.9%)—in all three categories—lends credence to the popular perception of their title. Nevertheless, the MI capital totals indicate an essentially flat market share in all three categories of the nine industry sectors.

Discussion

The results of this study indicate that a significant number of sectors in the U.S. music industry are in the initial stages of a decentralization cycle. Seven of the nine industry sectors under review show either stagnation or decline in growth rates and per capita shares for the U.S. music industry capitals. These data, viewed within the context of an expanding

U.S. music industry market, provides quantitative evidence of structuralchange in the industry.

It should be noted that many industry insiders do not consider the music industry to be decentralizing; instead, they describe it as a consolidation phase. For example, Verna’s (2003) interview with various major record label executives demonstrated that layoffs and cutbacks are the order of the day for their firms. However, these label executives’ perceptions may be rooted in their environment, for the major labels have lost significant market share over time. For example, Baskerville (1983) stated that major label market share in the 1980s exceeded ninety percent with the independent labels having approximately five percent worldwide. Two decades later, the major record label market share has shrunk to seventy percent with indie label shares approaching thirty percent (Verna 2003). Some economists would interpret this data as an indication of decentralization within the record industry as a whole, and corporate consolidation within the major labels. Additionally, decentralization theorists would postulate that the majors are declining in prominence and the independent labels are begin-ning an ascendancy phase. Finally, because an industry sector can apparently experience decentralization and consolidation cycles simultaneously within its membership, it is also conceivable that the aforementioned may be occurring at the intra-sector level.

It was noted earlier that the broadcast sector’s losses had a significant negative impact on the growth rates and revenue outputs of the music industry as a whole. Therefore, this researcher determined to gather supplemental information on the subject.

The Radio Advertising Board (RAB), the sales and marketing arm of the radio industry in the U.S., has published research and statistical data that are relevant to this study. In 2001, the RAB (2001) reported a 23% decline in national revenues for the radio industry, due mainly to the September 11 attacks on the United States. However, eighteen months later, radio broadcast revenues were reported to have recovered by 17% (RAB 2003). It should be noted that the RAB data confirm the accuracy of the Taylor and Terrell (2004) instrument, for this study’s data showed a 22.55% decline in revenues for the U.S. Broadcast sector.

However, the RAB research and data failed to address this study’s finding that the MI capital broadcast sector experienced a comparatively smaller decline in revenues (-7%) during this period. To this end, William McDowell, Vice President of Research for RAYCOM Media, was interviewed by the author. After reviewing the aforementioned data, and RAB research, McDowell explained that current radio revenues have now returned to their pre-September 11 levels. He considers the MI capital figures in broadcast to reflect the “unanticipated consequences of deregulation in the telecommunications industry” (Terrell 2005). Additionally, McDowell postulates that after the passage of the 1996 Telecommunications Act the large media conglomerates were able to own a larger number of radio stations in multiple markets. Given that most corporate headquarters of the media conglomerates are located in MI capitals, syndicated ad revenues from the secondary market stations bolstered their bottom lines (Terrell 2005). In summary, McDowell considers the radio industry to be in a consolidation mode caused by Federal Communications Commission (FCC) deregulation. Finally, the apparent consolidation cycle of the broadcasting sector contradicts Taylor and Terrell’s (2004) prediction that FCC deregulation would cause decentralization in the broadcast sector.

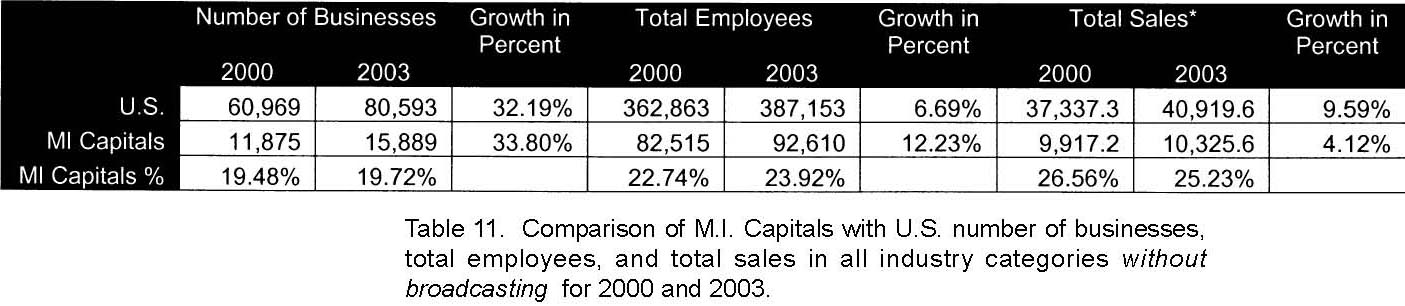

Given the aforementioned, this researcher presents the following to examine the state of the music industry and its capitals without the inclu-sion of the broadcast sector data. Table 11 shows that the U.S. and MI capitals had positive growth in all three sector categories. The MI capitals had a slightly higher growth rate in number of businesses and employees, but the U.S. had more than twice the growth rate in sales. As in Table 10, the MI capitals were found to have greater per capita shares in all three sector categories. However, the MI capitals’ market shares are either flat, or trending negative, in all of the three categories.

An overview of MI capital performance trends (market share) shows a declining prominence in recording, live entertainment, music retail, and creative services—and essentially no change in record retail and publishing. Seven of the nine industry sectors show evidence of decentralization while the others—publishing and broadcasting—are in a consolidation cycle. With modest revenue growth (4.12%) compared with the rest of the nation’s music industry (9.59%), the MI capitals may have difficulty maintaining their industry presence over time. For during periods of structural change, there will always be winners and losers.

Decentralization in this initial stage, is not so much the vacating of businesses from the MI capitals as it is simply a stagnation of the industry within the capitals combined with more robust growth in other areas of the country. However, if this trend continues it is reasonable to conjecture that some MI capital businesses and industry personnel might eventually relocate to areas where greater profits and larger salaries are possible. If this relocation occurs, the decentralization process will have entered the second stage of its cycle. The third stage of the decentralization cycle is implied in Garofalo’s (1999) historical analysis of the music industry. His accounting of the birth of the indie labels in the 1940s showed the sowing of the seeds of the new majors. For example, Atlantic Records is now part of the Warner/ Electra/Atlantic (WEA) distribution group—one of “The Big Four” labels. Finally, if this hypothetical decentralization cycle continues, a new group of major record labels, talent and management agencies, recording studios, etc. will emerge to replace the current major players—as per Garofalo’s analysis. Nevertheless, Werbach’s (2002) observation that decentralization is neither automatic nor absolute is relevant to this scenario. The new major players will inevitably seek to enhance their market share through mergers and various other forms of acquisitions (i.e., consolidation) and thus complete the cycle.

History shows that the music industry, as with other business structures, has experienced periods of decentralization followed by a consolida-tion phase. Many factors have been shown to precipitate decentralization cycles. Some of these factors are beyond an industry’s ability to foresee or control; therefore, predicting decentralization cycles is at best difficult. It is, however, possible to determine what type of company would best be able to adapt to these structural changes when they do occur. McGovern’s (Malone 2003) proposed model of groups of small autonomous companies can provide numerous adaptive advantages when compared to the large corporate model. These advantages include the ability to broker temporary collaborations within their circle or, when needed, outsource task assignments with firms outside their group. It is therefore possible for a group of companies to offer clients a wider range of products and services at competitive price points. During a decentralization cycle, company associations can realign their membership to adapt to new business demands. When this business model is compared with large corporate models (that must endure wasteful downsizing, retooling, etc.) the McGovern model is more adaptive, resilient, and efficient. Finally, during industry consolidation cycles, these company groups can survive—if not thrive—by developing niche markets and staying “under the radar” of the large predatory corporations.

In summary, the findings of this study confirm many of the results of Taylor and Terrell (2004). Most of the industry sectors in this study are shown to be in the initial phase of a decentralization cycle, and the others are in consolidation mode. This study confirms Taylor and Terrell’s 2004 postulation that the record industry is no longer the dominant force of the music industry (as of 2000, U.S. record retail employees and sales are now a distant second to broadcast radio). FCC deregulation policies are driving the current consolidation of broadcasting. The publishing sector has historically been a very closed community; therefore, its natural tendency is consolidation. More research is needed to determine why this sector seems so impervious to decentralization.

The music industry is not a monolithic structure; it is a group of businesses with only periodic common interests and goals. Intra-sector competition, as opposed to cooperation, has been the most frequently observed practice. The history of this industry teaches us that it reacts slowly to change. If the music industry is to compete successfully for the entertainment dollars of the U.S. consumer in the twenty-first century, it must learn to adapt more quickly to the various forces that impact it. Decentralization and consolidation cycles are indeed challenges, but they also present opportunities to those with the abilities to understand these cyclic phenomena and to adapt to them quickly.

Finally, the results of this study have important implications for music industry education in the United States. This author recommends that, as professors of music industry revise their institution’s curricula to address contemporary developments, they consider adopting the following changes if they are not already in place.

1) Provide entrepreneurial instruction in industry sectors experiencing growth on the national level;

2) Teach recording technology students musical, technical, and managerial skills appropriate for the operation of project studios, as opposed to preparing them for work in a higher echelon recording facility; and

3) Music industry programs not located in industry centers should begin (if they have not already done so) developing internships at local and regional independent labels, project studios, music stores, instrument manufacturers and wholesalers, artist management and talent agencies, and radio stations.

Table 1. Comparison of M.I. Capitals with U.S. Recording Studios for 2000and 2003.

* Sales figures are represented in million dollar units.

Table 2. Comparison of M.I. Capitals with U.S. artists’ managers and agents for 2000 and 2003.

* Sales figures are represented in million dollar units.

Table 3. Comparison of M.I. Capitals with U.S. bands, orchestras, actors,and other entertainment groups for 2000 and 2003.

* Sales figures are represented in million dollar units.

Table 4. Comparison of M.I. Capitals with U.S. record and pre-recordedproduct outlets for 2000 and 2003.

* Sales figures are represented in million dollar units.

Table 5. Comparison of M.I. Capitals with U.S. musical instrument storesfor 2000 and 2003.

* Sales figures are represented in million dollar units.

Table 6. Comparison of M.I. Capitals with U.S. musical instrumentmanufacturers/wholesalers for 2000 and 2003.

* Sales figures are represented in million dollar units.

Table 7. Comparison of M.I. Capitals with U.S. licensing, royalties, andpublishing services for 2000 and 2003.

* Sales figures are represented in million dollar units.

Table 8. Comparison of M.I. Capitals with U.S. creative services for 2000and 2003.

* Sales figures are represented in million dollar units.

Table 9. Comparison of M.I. Capitals with U.S. broadcast services for2000 and 2003.

* Sales figures are represented in million dollar units.

* Sales figures are represented in million dollar units.

* Sales figures are represented in million dollar units.

References

Balovich, David. “Centralization vs. Decentralization Takes

on a Whole New Meaning.” Creditworthy News (August 27, 2003)

Baskerville, David. Music Business Handbook and Career Guide. 1st ed. Thousand Oaks, Calif.: Sherwood Publishing, 1983.

Clark, Rick. “Radio! Radio!” Mix 27, no. 6 (May 2003): 94–96.

Dun & Bradstreet. Marketplace CD ROM. Natick, Mass.: Dun & Bradstreet, 2000.

Dun & Bradstreet. Marketplace CD ROM. Natick, Mass.: Dun & Bradstreet, 2003.

Fink, Michael. Inside the Music Industry: Creativity, Process, and Business. 2nd ed. New York: Schirmer Books, 1996.

Franklin, Ron. “Up, Down, All Around: Pro Audio Manufacturing at the Crossroads.” Mix 27, no. 6 (May 2003): 112–118.

Garofalo, Reebee. “From Music Publishing to MP3: Music and Industry in the Twentieth Century.” American Music, Fall 1999.

Gray, André. “The

Demo Report 2004.” Digital & Electronic Music Organization, Inc.

(2004)

Kropotkin, Peter. The Conquest of Bread. New York and London: G. P. Putnam’s Sons, 1906.

Krumme, Gunter. “Corporate Growth Through Spatial Decentralization: Triumph’s Expansion Path.” International Geographical Union Congress 1 (1972): 554–566.

Malone, Thomas. “The Decentralization Imperative.” MIT Technology Insider, September, 2003.

McDowell, William. Personal interview with Dr. William McDowell of RAYCOM Media. May 23, 2005.

Radio Advertising Board. Radio

Proves Critical Source of News and Information for Nation even as

September Ad Revenues Slump (November 7, 2001)

Radio Advertising Board. Radio

Revenues Soar 17% in September, Marking the Largest Monthly Increase

Since 2000: Continued Growth for 4th and 1st Quarter on the Horizon

(November 19, 2003)

Shore, Laurence Kenneth. “The Crossroads of Business and Music: A Study of the Music Industry in the United States and Internationally.” Dissertation. Ann Arbor, Mich.: UMI Dissertation Services, 1983.

Taylor, Frederick, J. and Phillip, A. Terrell. “An Analysis of Economic Trends in U.S. Music Industry Capitals: 1995-2003, with Implications for Music Industry Education.” MEIEA Journal 4, no. 1 (2004): 105–135.

Taylor, Frederick, J. and Phillip A. Terrell. “A Comparison of Five American Music Industry Centers of Commerce.” Southern Business and Economic Journal 25, nos. 3 and 4 (Summer/Fall 2002): 244–259.

Terrell, Phillip A. “Digital Audio in U. S. Higher Education Audio Recording Technology Programs.” Dissertation. Georgia State University, 2001.

- U.S.

- Census Bureau. 2000

Census Report. Washington, D.C.: U.S. Census Bureau (2000)

- U.S.

- Department of Commerce. North American Industry Classification System (Version 1.0 CD ROM). Springfield, Virginia: Office of Management and Budget’s Economic Classification Policy Committee, 1997.

Verna, Paul.

“Record Label Remedy.” Mix 27, no. 6 (May 2003): 42–55.

Werbach, Kevin. “Tech’s Newest Trend—Decentralization.” ZDNet News (October

24, 2002)

PHILLIP TERRELL is Director of Music Industry Studies at Alabama State University. His industry experience includes serving as a recording studio owner/manager and engineer, talent agent, music store assistant manager, touring and session guitarist, and national sales representative for an audio console manufacturer. Dr. Terrell has taught music business and recording technology at Georgia State University, Northeastern University, and Albany State University.

He has a bachelor of music degree from Mercer University Atlanta, a master of music degree from Georgia State University, and a Ph.D. in higher education/music industry from Georgia State University. Dr. Terrell’s research interests are music industry economic impact studies, artificial intelligence applications in digital audio workstations, and jazz guitar history and techniques. His professional memberships include the National Association for the Study and Performance of African American Music Board of Directors, National Academy of Recording Arts and Sciences, National Association of Music Merchants, and Music and Entertainment Industry Educators Association.